The time is ripe for investors to invest selectively in private equity.

As an asset class, private equity has become more mainstream over the past 10 years, due to a broadening investor base, easier access and increased allocations among investors seeking strong returns amid ongoing volatility in public markets.

1 Source: Preqin Future of Alternatives 2028

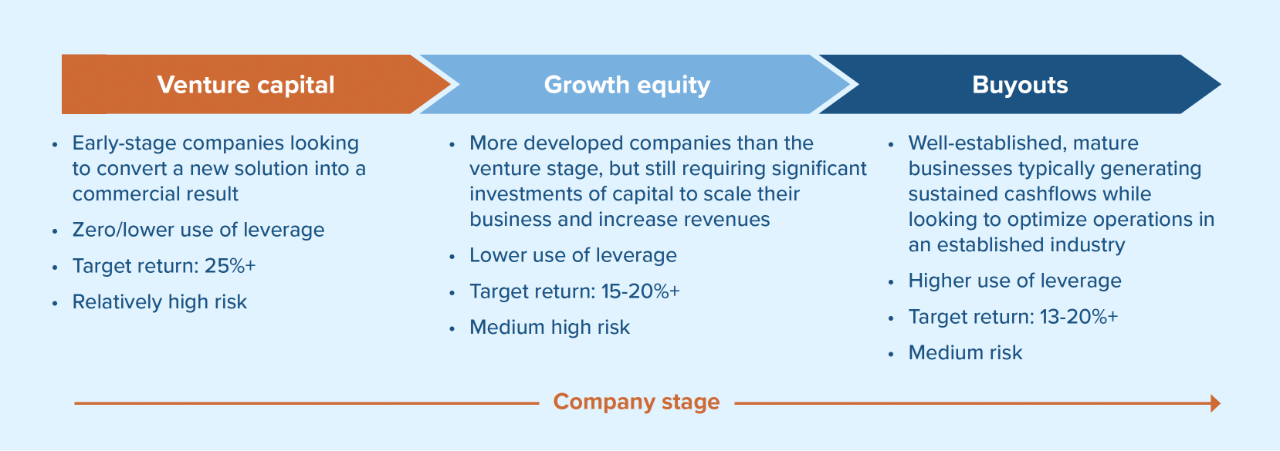

While private equity investing has been around for decades, many new investors are less familiar with what goes on within the asset class. There are three broad private equity segments, each with different risk and return opportunities.

For illustrative purposes only. Target return information is provided for general guidance and should not be relied upon when making investment decisions

For illustrative purposes only. Target return information is provided for general guidance and should not be relied upon when making investment decisions

These segments experience different trends over time as capital and liquidity conditions in the markets evolve. With the emergence of higher interest rates, inflation and uncertainty about the elusive “soft landing”, gone are the days of ultra-low borrowing costs and the associated sky-high valuations for riskier venture and growth companies. As a result, over the past two years investor attention and capital flows shifted from the venture segment into buyout, toward companies that are already profitable, are generating free cash flow and have already proven to be viable.

In addition to different segments within private equity, there are also different ways to invest in private equity:

- Direct investing: The investor purchases equity directly in a private company.

- High minimum investment but potentially high payout

- Highly concentrated approach dependent on one company’s success

- Primary investing: A private equity manager builds a fund and collects capital from investors to buy a group of private companies. Investors becomes unitholders in that fund and benefit from active management, growth, and transformation of the private companies within the fund.

- Focused on long-term value creation through operational improvement

- Secondary investing: The investor buys another party’s existing commitments to private equity funds partway through the fund’s value creation cycle.

- Earlier cash flows and the ability to invest in de-risked assets

Along with the shift toward the buyout segment, there has been rapid growth in secondary investing, driven by the overall growth of the private equity landscape, a slowdown in initial public offering activity in 2023, volatility in the public markets and the ongoing desire of private equity investors for liquidity. This has created a fertile environment for managers skilled in navigating the opportunities currently on offer in the private equity secondary market.

Considering all this, there is a tremendous opportunity for advisors to help their clients take advantage of this transition and pivot their investments toward the parts of the market that are on the rise and are likely to sustain performance as long as interest rates remain elevated, which is expected for the foreseeable future.

Benefits of private equity

Historically, private equity has offered a return advantage over public markets. This asset class has delivered mid-teen annual returns — several percentage points ahead of public equity markets — over the past quarter century.

Source: Northleaf and Morningstar. Returns in CAD, as of December 31, 2023. Northleaf Private Equity includes all fund investments and direct co-investments made by Northleaf’s global solutions funds and discretionary global solutions custom mandates from the launch of TD Capital/Northleaf’s first global solutions fund in 2002. Northleaf Private Equity excludes investments made by Northleaf’s custom mandates with specific geographic restrictions (Northleaf’s Canada-focused custom programs, Ontario Venture Capital Fund and Northleaf Venture Catalyst Fund).

Additionally, private equity has been an attractive option for investors because it comes with lower volatility, especially when markets are weak and public markets are falling. This is in part because private equity is usually valued only once per quarter, providing less motivation for investors to sell at inopportune times, which would lock in losses.

Source: Private equity data provided by Cambridge Associates. Public market indices provided by Morningstar Direct. Private Equity: Cambridge U.S. Private Equity Index (Legacy). Data denominated in CAD. Private equity returns are shown net of fees, expenses and carried interest. Past performance is not indicative of future performance

Skilled private market investors can also find plentiful investment opportunities because the world of private companies is considerably larger than the public sphere. In fact, over 97% of companies with more than $10 million in annual revenue are privately held, making it impossible to invest in them via the public markets.

Finally, private equity can bring more diversification benefits to investors’ portfolios because there is less correlation to traditional asset classes, potentially resulting in a more balanced and well-constructed portfolio over time.

Understanding liquidity in portfolios

Advisors should help their clients understand that one of the main differences between private and public investing is the amount of liquidity available.

Unlike in public markets, private equity investors do not have the flexibility to immediately sell their holdings in private equities and move on to different investments. Traditional private equity funds are structured as closed-end funds. Investment capital is raised during an initial fundraising period and called from investors as opportunities are identified. Private companies are bought, improved over time and sold at a (hopefully) significant profit five to 10 years later. Through this process, investors achieve liquidity over a longer period, as companies are sold following value creation and capital gains are returned to investors periodically throughout a typical 10-year fund life. A properly diversified fund with many companies held by several private equity funds offers the best chance of regular liquidity for investors.

Advisors should make their clients aware that this asset class is best-suited for investors who have a longer time horizon, as their ability to redeem their funds will be limited. The upside, of course, is that this limited liquidity is generally compensated with a higher expected return — also known as an “illiquidity premium.”

With private equity rapidly growing in demand, this asset class is becoming impossible for advisors and their clients to ignore. To ensure clients’ portfolios remain diversified, it is important for advisors to be aware of and stay up to date on the evolution and opportunities that exist within the space and to identify managers and strategies that can effectively capitalize on these trends.

Learn more about Mackenzie Northleaf Global Private Equity Fund.

Explore all Mackenzie Northleaf private market offerings.

For accredited investors only (as defined in NI 45-106). Past performance is not necessarily indicative of any future results.

The content of this web page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This material is not intended to constitute an offer of units of Mackenzie Northleaf Global Private Equity Fund (the “Fund”). The information herein is qualified in its entirety by reference to the applicable Offering Memorandum of the Fund. The OM contains information about the investment objectives and terms and conditions of an investment in the Fund (including fees) and also contains tax information and risk disclosures that are important to any investment decision regarding such Fund.